In today's financial landscape, understanding the nuances of retirement accounts is crucial for long-term wealth building. One key aspect that often gets overlooked is the Spouse Roth IRA contribution. This financial tool allows married couples to enhance their retirement savings strategy effectively. In this article, we will explore the ins and outs of Spouse Roth IRA contributions, detailing eligibility criteria, benefits, and strategies to maximize your contributions.

The Spouse Roth IRA is a unique option that provides couples with the flexibility to save for retirement even if one partner does not have earned income. This feature makes it an ideal choice for stay-at-home spouses or those taking a break from the workforce. By leveraging this account, couples can ensure that both partners have sufficient funds for a comfortable retirement.

Throughout this guide, we will dive deep into the mechanics of Spouse Roth IRA contributions, including how to open an account, contribution limits, and tax implications. Whether you are just starting your financial journey or looking to optimize your existing retirement strategy, this article will serve as your comprehensive resource.

Table of Contents

- Understanding Spouse Roth IRA

- Eligibility Criteria for Spouse Roth IRA Contributions

- Benefits of Contributing to a Spouse Roth IRA

- Contribution Limits for Spouse Roth IRA

- Tax Implications of Spouse Roth IRA Contributions

- Strategies to Maximize Your Spouse Roth IRA Contributions

- Common Mistakes to Avoid When Contributing

- Conclusion

Understanding Spouse Roth IRA

A Spouse Roth IRA is a type of retirement account that allows a working spouse to make contributions on behalf of a non-working spouse. This feature is particularly beneficial in households where one partner may be taking care of children or pursuing education, thus not earning an income. By contributing to a Spouse Roth IRA, couples can effectively double their retirement savings potential.

Eligibility Criteria for Spouse Roth IRA Contributions

To qualify for Spouse Roth IRA contributions, both spouses must meet certain conditions:

- Both spouses must file a joint tax return.

- The working spouse must have earned income that is at least equal to the total contributions made to both Roth IRAs.

- Contributions are subject to income limits which can affect eligibility.

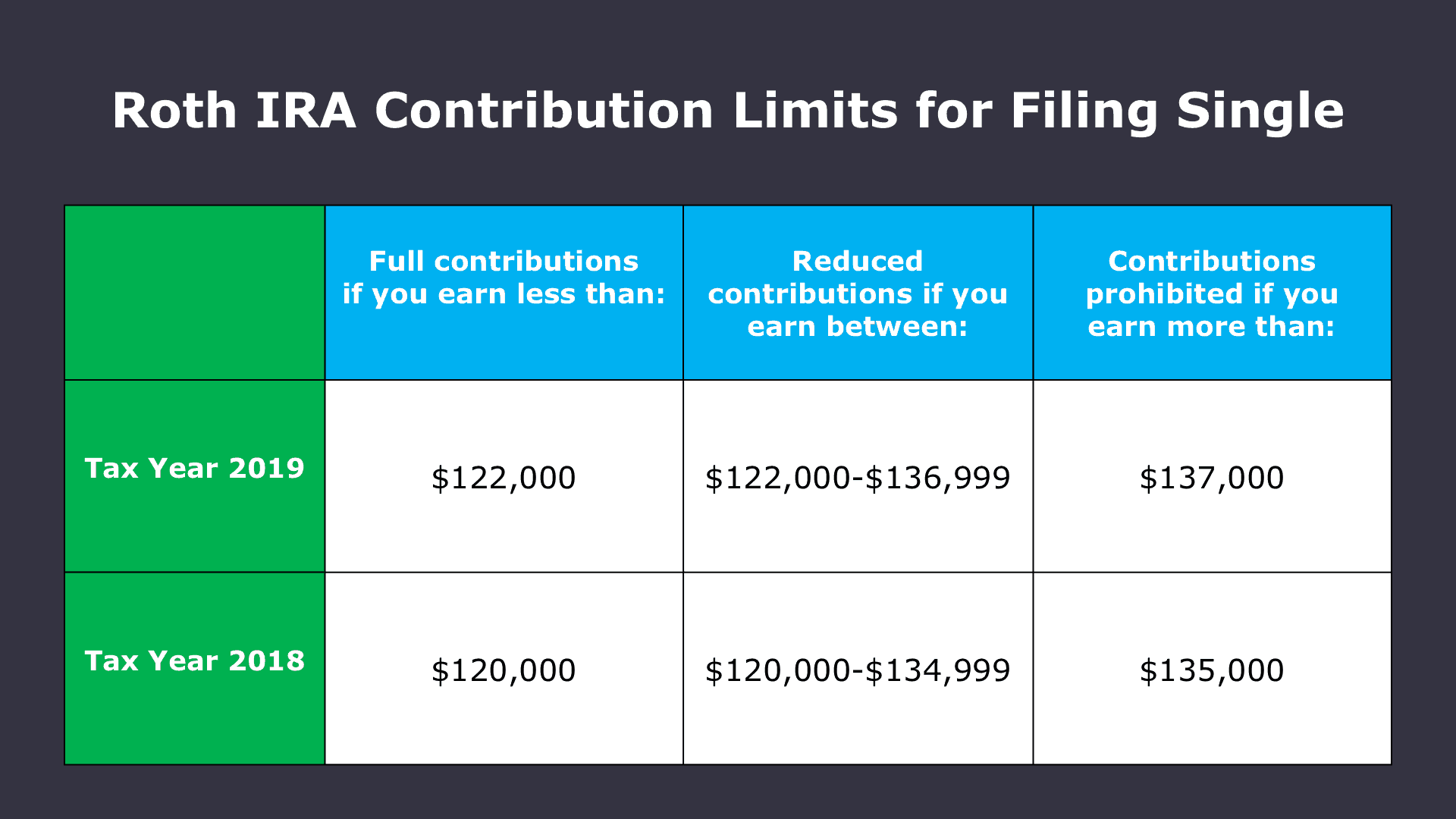

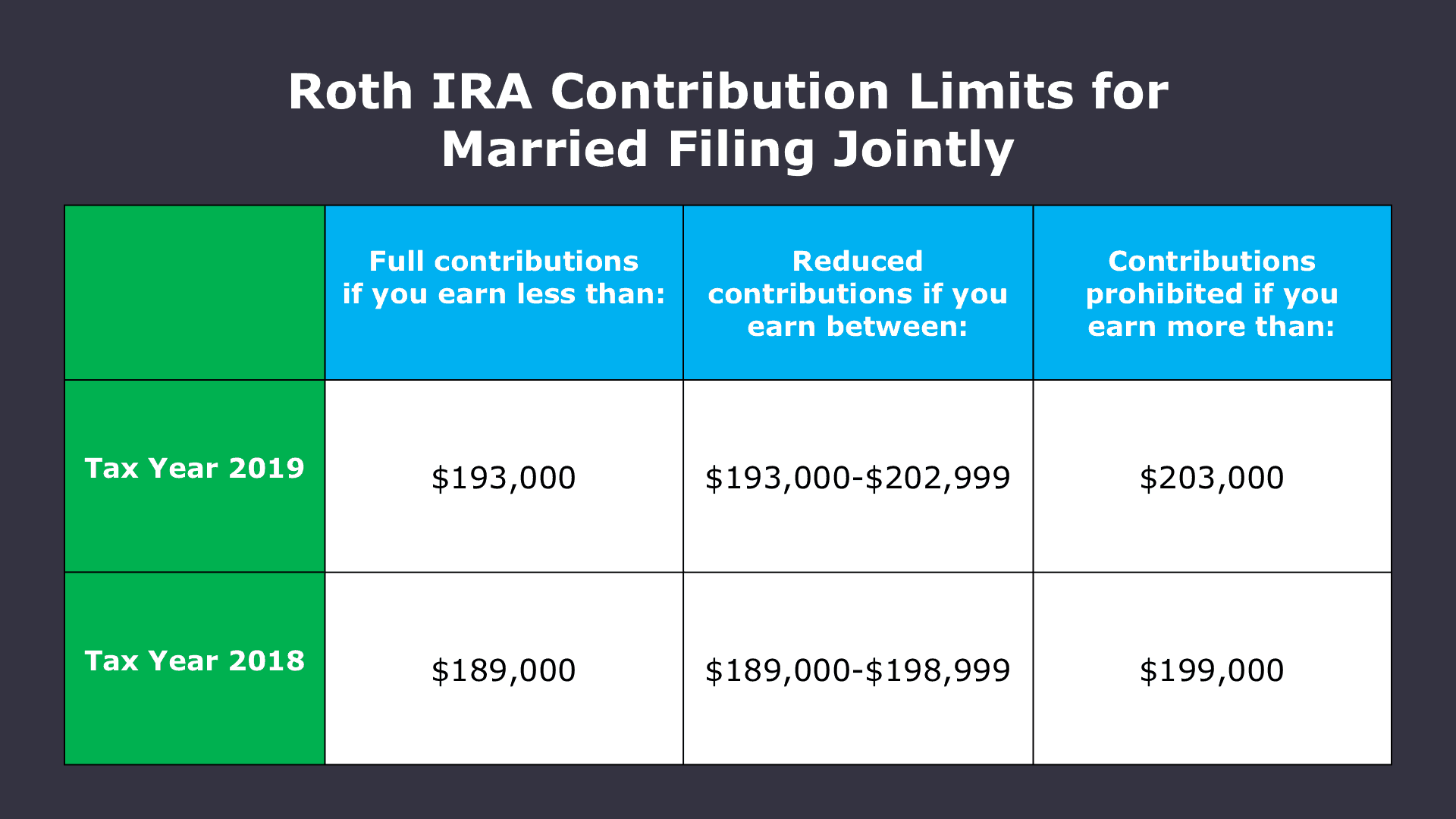

Income Limits for Roth IRA Contributions

As of 2023, the income limits for contributing to a Roth IRA are as follows:

- Single filers: Modified Adjusted Gross Income (MAGI) must be less than $140,000 to contribute the full amount.

- Married filing jointly: MAGI must be less than $208,000 for full contributions.

- For incomes above these thresholds, contributions may be reduced or phased out completely.

Benefits of Contributing to a Spouse Roth IRA

There are several advantages to contributing to a Spouse Roth IRA:

- Tax-Free Growth: Contributions grow tax-free, and qualified withdrawals are also tax-free.

- Flexibility: Withdraw contributions at any time without penalties or taxes.

- Retirement Security: Increases the overall retirement savings of the couple.

Contribution Limits for Spouse Roth IRA

For the tax year 2023, the maximum contribution limit for a Spouse Roth IRA is:

- $6,500 per individual per year, with an additional catch-up contribution of $1,000 for individuals aged 50 and older.

- Both spouses can contribute to their individual Roth IRAs, effectively allowing a total contribution of $13,000, or $14,000 if both are aged 50 or older.

Tax Implications of Spouse Roth IRA Contributions

Contributions to a Spouse Roth IRA are made on an after-tax basis, meaning you do not receive a tax deduction for the contributions. However, the tax implications provide significant benefits:

- Tax-free withdrawals during retirement.

- No required minimum distributions (RMDs) during the account holder's lifetime.

- The ability to pass on tax-free growth to heirs.

Strategies to Maximize Your Spouse Roth IRA Contributions

To make the most out of your Spouse Roth IRA, consider the following strategies:

- Automate Contributions: Set up automatic transfers to ensure contributions are made consistently.

- Make Catch-Up Contributions: If you or your spouse are over 50, take advantage of catch-up contributions.

- Invest Wisely: Choose a diversified investment strategy to maximize growth potential.

Common Mistakes to Avoid When Contributing

When managing a Spouse Roth IRA, it's essential to avoid common pitfalls:

- Failing to meet income limits.

- Incorrectly assuming contributions are tax-deductible.

- Neglecting to track contributions to avoid exceeding limits.

Conclusion

In summary, the Spouse Roth IRA is a valuable tool for married couples looking to enhance their retirement savings. By understanding eligibility criteria, benefits, and strategies for maximizing contributions, you can secure a more comfortable financial future for you and your spouse. Don't hesitate to consult with a financial advisor to tailor a plan that works best for your unique situation.

We encourage you to leave a comment below with your thoughts on Spouse Roth IRA contributions or share your experiences. If you found this article helpful, consider sharing it with friends or exploring other informative articles on our site!

Thank you for reading, and we hope to see you back soon for more insights on personal finance and retirement planning!

You Might Also Like

Cozumel Vacation Rentals: The Ultimate Guide For Your Dream GetawaySutter Urgent Care Auburn: Your Comprehensive Guide To Quality Healthcare

Understanding StockTwits TSLA: A Comprehensive Guide To Tesla's Stock Sentiment And Market Trends

AudiobooksBee: The Ultimate Guide To Enjoying Audiobooks In 2023

Exploring The World Of Scuffed Entertainment: A Deep Dive Into Its Impact And Popularity

Article Recommendations